Prices

Palladium market overview

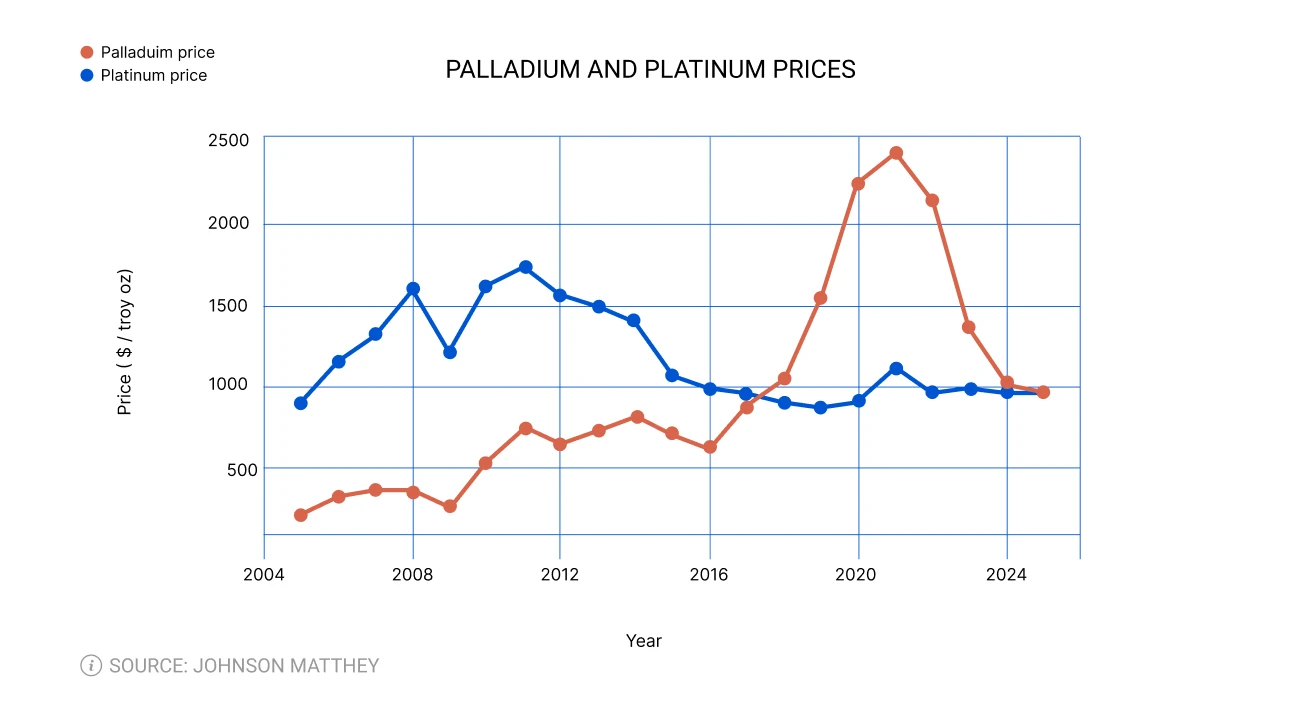

Palladium is the most produced metal among the platinum group metals (PGMs). Unlike other PGMs, its extraction is less concentrated and primarily takes place in two major regions – South Africa and Russia. This diversified supply chain reduces the risk of significant disruptions and ensures a more stable flow of palladium to the market. As a result, palladium generally has a lower average price compared to other PGMs.

Historical trend

Over the past 20 years, palladium has demonstrated a steady upward trend in value, driven by consistently increasing demand from the automotive industry, which traditionally accounts for approximately 80% of total palladium consumption. The rising demand has been fuelled by stricter environmental regulations in various countries, as lower permissible emission levels have forced automakers to increasingly rely on palladium-based catalytic converters to comply with new standards.

The period that disrupted the stable trend was 2020–2024, when a series of supply shocks led to heightened volatility in the palladium market, as well as for other PGMs. This period was marked by supply chain disruptions caused by the COVID-19 pandemic, a major technical accident at Russia’s leading producer, and overall geopolitical instability.

Conclusions and forecasts

Currently, the palladium market has stabilised after the shock period of 2020–2024, with prices fluctuating within the range of $900–1,100 per ounce. According to analytics, this price level is expected to persist in the near future with a slowdown in the mid-term due to trends in the automotive industry, which is gradually shifting towards electric vehicles, and growing recycling volumes. However, it is also noted that a growing share of petrol-powered internal combustion engines, which require more palladium compared to diesel engines, and new applications in alternative energy and high-tech industries, will protect the market from strong price volatility.